GOOD MORNING!

FOREX

Most currencies are trading strong against the Dollar Index which might trade between 100-99.40 for the near term with an eventually rise beyond 100 in the coming days while Euro can attempt to test 1.16 before coming down towards 1.15. , USDJPY has recovered well and looks poised to test 160 and higher soon while EURJPY can slowly rise towards 185-160 region. Aussie and Pound can test 0.71-0.72 and 1.35+ before facing rejection from there. USDCNY can target 6.70 in the near term while below 6.75. USDINR could trade below 95.50.

Dollar Index (99.74) looks steady in the 99.40-100 region. A rise above 100 is needed to confirm initial strength in the index and to ensure eventual rise towards 100.50-101. The overall medium term trend is to the upside.

EURUSD (1.1546) could extend to 1.16 in the coming days with immediate downside limited to 1.15. A break below 1.15 would be needed for the Euro to resume its downtrend.

Dollar-Yen (159.13) has broken abive 159 as expected. A slow and steady rie back towards 160 and higher can be achieved soon.

EURINR (110.1707) is bullish above 110 for a slow rise to 110.50 or higher while EURJPY (183.74) has risen above 183 and can soon head towards 184.

USDCNY (6.7444) is sustaining trade below 6.75 and if it continues, we could see a dip towards 6.70 soon.

Aussie (0.7060) is holding well above 0.70 and while the rise sustains, a slow upmove could be established towards 0.71 initially and then 0.72 in the longer run.

Pound (1.3513) is attempting to sustain trade above 1.35 and while that succeeds, we may expect a slow and steady rise towards 1.375 or higher in the next 1-2 months.

USDINR (95.31) traded higher yesterday contrary to our expectations of seeing a dip towards 95.00. We may expect a stable trade below 95.50 in the near term.

INTEREST RATES

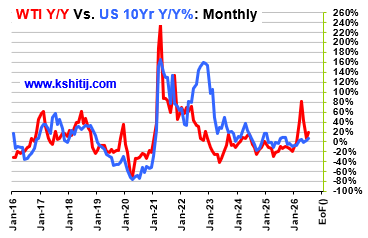

The US Treasury Yields are moving up in line with our expectation. They can rise further from here and test their resistance. A short-lived correction is possible thereafter. The US CPI data release tomorrow will need a close watch. The German Yields have got a good follow-through rise. That keeps intact our bullish view. The yields can rise more. The 10Yr GoI is still stuck inside the narrow range. We expect it to break the range on the downside and fall going forward.

The US 10Yr (4.71%) and 30Yr (5.25%) yields are heading up towards 4.8% (10Yr) and 5.35%-5.4% (30Yr) in line with our expectation. A short-lived correction is a possibility thereafter. Support is at 4.6%-4.55% (10Yr) and 5.15%-5.1% (30Yr)

The German 10Yr (3.18%) and 30Yr (3.67%) Yields have risen further. That keeps intact our bullish view of seeing 3.3%-3.35% (10Yr) and 3.8% (30Yr).

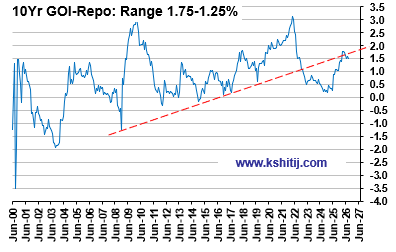

The 10Yr GoI (6.7633%) remains stable inside the 6.75%- 6.8% range. While below 6,.8%, the bias is negative to break 6.75% and fall to 6.7% first and then to 6.6%.

STOCKS

Dow is likely to remain range-bound within the 53000-55000 range for some time. DAX remains bullish above 26000 and can rise towards 27000 if it breaks sustainably above 26500. Nifty continues to hold above the key 24500 support and can advance towards 24800-25000 in the coming week. Nikkei remains strong and can extend its rally towards 68000-70000. Shanghai also continues to strengthen and can rise further towards 4000-4050 in the near term.

Dow (54053.38, -0.02%) could continue to trade within the broad range of 53000-55000 for some time.

DAX (26433.18, +0.03%) needs a sustained break above 26500 to extend the rally towards 27000 or higher. While the immediate support at 26000 holds, the rise towards 27000 remains likely.

Nifty (24,583.80, +0.05%) is holding above 24500. While it sustains above this level, a further rise towards 24800-25000 looks likely over the coming week.

Nikkei (67130.91, +0.56%) is rallying higher in line with our expectations and can rise further towards 68000-70000 in the near term.

Shanghai (3957.80, -0.22%) is moving higher in line with our expectations and can rise further towards 4000-4050 in the near term.

COMMODITIES

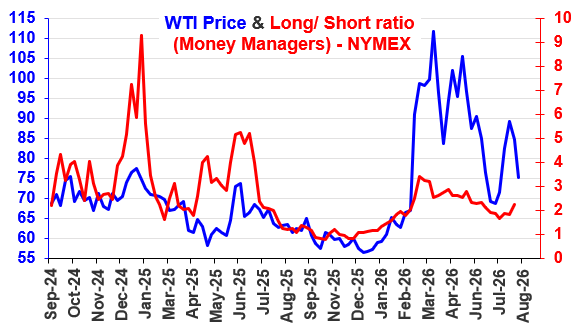

Brent and WTI are likely to remain range-bound within $80-$100 and $75-$90 respectively. Gold remains strongly bullish and can rise further towards $4500-$4550, while Silver continues to strengthen with scope to advance towards $65-$70. Copper has seen a mild recovery but remains vulnerable to a decline towards $6.50-$6.45. Natural Gas remains constructive above the key $2.60 support and can rise further towards $2.80-$3.00 in the near term.

Brent ($87.83) and WTI ($82.21) are moving sharply higher and are likely to remain volatile and broadly range-bound between $80-$100 and $75-$90 respectively for some time.

Gold ($4479.30) is moving higher in line with our expectations and can rise further towards $4500-$4550 in the coming sessions.

Silver ($66.06) is also moving higher in line with our expectations and can advance further towards $65-$70 in the coming sessions.

Copper ($6.65) has recovered slightly but remains vulnerable to a decline towards $6.50-$6.45 in the coming sessions.

Natural Gas ($2.7740) can rise further towards $2.80-$3.00 in the near term while it holds above the support at $2.60.

DATA TODAY

4:30 10:00 RBA Meeting

...Expected 4.35 % ...Previous 4.35 %

14:00 19:30 US Existing Home Sales

...Kshitij Expn 4069 K ...Expected 4050 K ...Previous 4090 K

DATA YESTERDAY:-

----------------

No major data release yesterday.

DISCLAIMER

These views/ forecasts/ suggestions, though proferred with the best of intentions, are based on our reading of the market at the time of writing. They are subject to change without notice.Though the information sources are believed to be reliable, the information is not guaranteed for accuracy. Those acting in the market on the basis of these are themselves responsible for any profits or losses that might occur, without recourse to us. World financial markets, and especially the Foreign Exchange markets, are inherently risky and it is assumed that those who trade these markets are fully aware of the risk of real loss involved.

WARNING !!

Visitors should be aware that Foreign Exchange transactions and trading are or can be subject to laws, rules and regulations of the country in which the entity undertaking the transactions is situated. It is incumbent upon the Visitors to keep themselves informed and abreast of the Laws they are (or would be expected to be) subject to and governed by, and act in accordance thereto.